What can you expect in 2024?

Investment matters - What to expect from 2024?

Thursday 11 January, 2024

A lot can change in a week in investment markets. Given this, a year can feel like a different era. In January 2023, we were in the middle of the sharpest increase in interest rates for decades and economists were expecting a recession in most developed countries. Roll on 12 months, investors are now looking ahead to interest rate cuts and, instead of recession, latest data showed the US economy continues to produce strong growth. Even the UK economy, which looked destined for a deep contraction, has held on to growth.

All of which highlights the challenges of making short-term forecasts and reiterates why we take a long-term strategic approach to investing. That said, it is important to understand what is driving short-term investor behaviours. So with that in mind, here are four key investment matters that we believe advisers and their clients should be paying attention to in 2024.

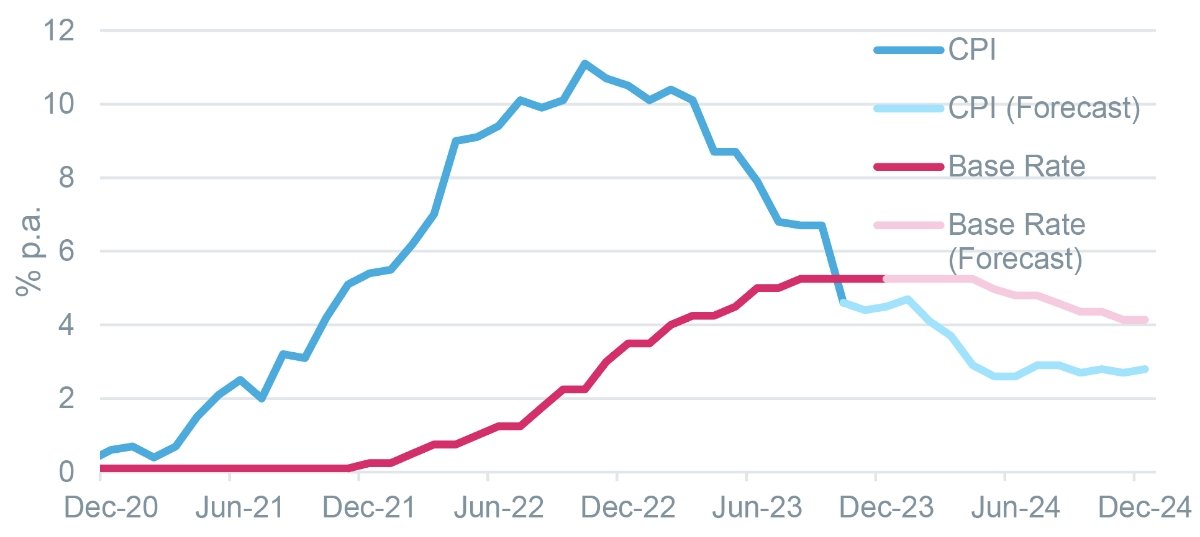

1. Inflation and interest rates are likely to remain top of investors’ agendas, but growth prospects are also important

Inflation has fallen considerably in the UK from its 11.1% peak, thanks in part to an aggressive policy of interest rate increases from the Bank of England. The job isn’t done yet, but only a few months after potentially the last rate hike, investors are already looking ahead to potential interest rate cuts in 2024. Once the major central banks of the world have pivoted from tightening to easing, investors’ attention may turn to what the impact of the tightening has been. Now, as much as ever, feels a sensible time for investment portfolios to be well diversified to capture the relevant market opportunities, but equally important to be insulated from the worst of any adverse market outcomes.

Interest rates are expected to fall as inflation approaches 2% target

Source: ONS, Bank of England, Consensus Forecasts

2. The expected fall in cash rates is likely to reduce the attractiveness of money market funds

Cash rates and flows into money market funds increased notably over 2023. Looking forward, we believe the strategic investment case for cash has decreased. Yes, cash rates are attractive now, but they are expected to fall during 2024. In addition, the expected return of assets, like bonds, are significantly higher than where they were 12-18 months ago.

3. Elections have the potential to increase short-term market volatility

There is huge potential for a change in the political wind, with over half the world’s population voting in more than 70 elections this year. Elections can impact markets in various ways. The uncertainty can lead to market volatility, especially when polls are tight (currently that’s a yes in the US and a no in the UK). Governments’ tendency to move toward more pro-growth policies in the lead-up to an election, to try and gain favour with the electorate, can sometimes be supportive for markets. But ultimately, over the longer-term, the evidence highlights that markets and economies will tend to be driven by stability and strong underlying economic fundamentals.

Risk warning

This communication is issued and approved by Lonsdale Services Ltd. It is based on its understanding of events at the time of the relevant preparation and analysis. The information and opinions contained in this document are provided by Lonsdale and are subject to change without notice and should not be relied upon when making investment decisions. The value of your investments and the income from them may go down as well as up and neither is guaranteed. Investors could get back less than they invested. Past performance is not a reliable indicatorof future results.

Changes in exchange rates may have an adverse effect on the value of an investment. Changes in interest rates may also impact the value of fixed income investments.

The value of your investment may beimpacted if the issuers of underlying fixed income holdings default,

or market perceptions of their credit risk change.There are additional risks associated with investments in emerging or developing markets. The information in this document does not constitute advice, nor a recommendation, and investment decisions should not be made on the basis of it. The material provided should not be released or otherwise disclosed to any third party without prior consent from Lonsdale.